Through all the Uncertainty, this remains the Same

April 2, 2026

Over the last several years we have chronicled the backdrop price inflation storyline from nearly every conceivable perspective. No matter how we sliced it, price inflation was a systemic issue.

As a citizen, you already know this. What about in more recent time?

Narratives built and consistently iterated and reiterated, in particular from various policymakers in D.C., have offered nearly ad nauseam that price inflation was conquered and finished off nearly a year ago. The topic, as a topic, is a non-topic, if I understand the narratives correctly.

Regardless, price inflation is a topic, regardless of X narrative(s) offering that it is nothing but a historical topic, at best.

Importantly, very importantly, this is before the most recent war. What has seemingly seeped into the collective narratives, relative to price inflation, is that the war will bring higher prices, but those will be temporary.

This implies, again, that indeed price inflation had been taken care of, such as the narrative(s) have offered. It was a thing, then it was finished off, and it will be arising to some degree again, but that too will be finished off quickly, post-war.

The problem with this is the data has not been cooperating with the narratives. (This is always the problem with narratives eh, pesky reality gets in the way of a good storyline.) In particular, when we view the Federal Reserve’s long-standing favored measure of price inflation.

The Personal Consumption Expenditure Chain-type Price Index has been their go-to price index for many years. There are certainly many other price measures to reference, but this is their go-to.

We have delved into their go-to index in previous editions, along with a plethora of other price measures. For today’s edition we’ll look at the core index for Personal Consumption Expenditures (PCE).

The core index is the PCE index without food and energy costs included. This is called a core measure because it extracts out the more volatile components, such as food and energy.

This is meant to aid in giving a view of what the price inflation trend looks like throughout the pricing structure, without the volatile components skewing the underlying price trends.

It is here, as well as in various other price inflation measures, that we can see the data is not cooperating with X narratives relative to this topic.

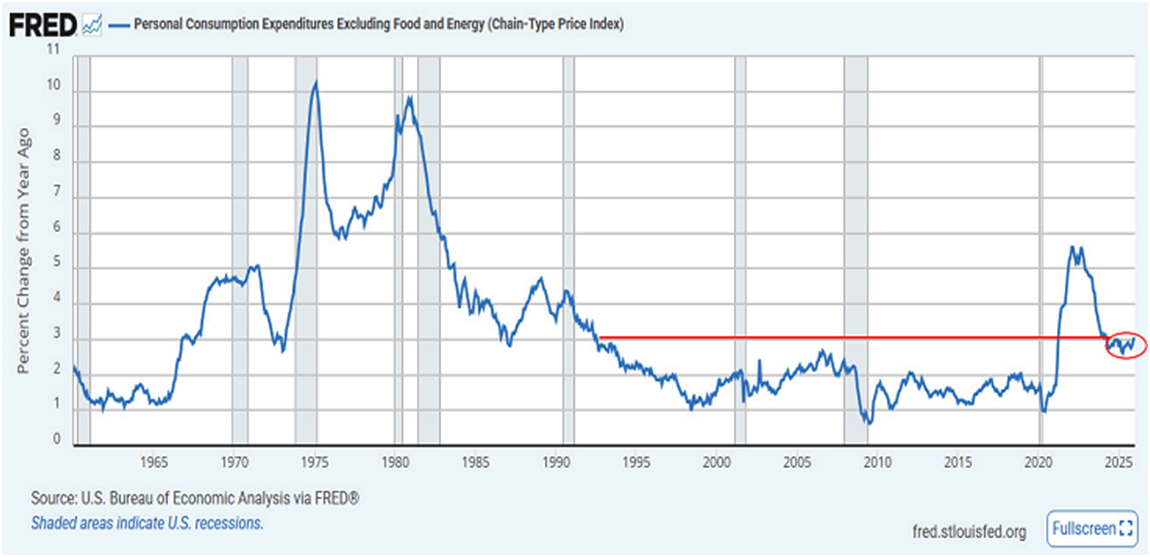

Click for Larger View: https://fred.stlouisfed.org/graph/?g=1TwfT

For some broad historical perspective, the above chart starts in 1960 and walks us up to the current day.

To emphasize how stubborn price inflation has been throughout our current price inflation era, dating back to 2021, we inserted a red horizontal line beginning in the early 1990’s.

Think of this red line as a well-established ceiling whereby this price measure was clearly unable to penetrate, or even touch, until our current price inflation era, whereby it easily shot through it to the upside.

In addition, we have added a red circle to emphasize the more recent behavior. The encircled period dates back to January of 2024 to the current day. Yes, two-plus years of time whereby the growth in this core price index has refused to trend lower, while in recent months it has begun to trend upward again.

We emphasize growth because it is far too easy to see the declining rate of growth and interpret it as a decline in prices. Let’s not forget, the decline from peak levels merely reflects that the growth in prices is lower than what it had been at its peak growth rate.

As the above measure stands, this PCE core price index is registering a 3.1% increase in year-over-year prices. This is quite a distance away from the Fed’s well-stated 2% price inflation target. Hence, why we insinuated above that X narratives’ offering price inflation is a non-topic is pure fantasy.

Importantly, all the above data reflect pre-war price growth trends. When, and if, you hear that prices are rising again because of the war, you may want to mentally consult the above data to realize prices had already been rising prior to the war.

The bottom line, as stated above, price inflation trends have not disappeared. The Fed has cut their benchmark Fed Funds rate six times, beginning in September of 2024 up to the current day.

Along that path, for our part, we had questioned the price inflation evidence to support a rate-cutting campaign. History offers cutting rates during a price inflation era, but assuming the price inflation issue had been dealt with does not end well.

This certainly was not lost on collective bond market participants as they raised various treasury notes and bond interest rates while the Fed was cutting. This is their way of offering disagreement with the policy approach of rate cuts before price inflation was fully extinguished.

The coming months should offer quite an interesting storyline across the plethora of price inflation measures. Right now, with the Fed’s favored measures not cooperating at all relative to their 2% price inflation target, those who hope for additional Fed rate cuts may be disappointed.

Then again, if more rate cuts do surface while price measures are not cooperating, we all may be disappointed, as citizens, as we deal with unfavorable price trends downstream. Cutting rates to curtail a price inflation era has proven to be nonsensical, historically speaking, and is seemingly proving to be the case in our current era.

I wish you well….

-Ken from Mind Your Stops