No Matter the Reason, This Will not Work for the Everyday Household

June 18, 2026

Over the years we have occasionally offered editions that have looked at the most important wage rate measure for the everyday household. It has been nearly two years since we have focused an edition on this important socioeconomic measure.

Underneath this measure, it elicits the old adage that it is not what you make that matters most, but what you keep.

That adage, historically speaking, usually spoke to taxes and how much the proverbial taxman took from household incomes.

If we widen the lane a bit relative to that adage, we can easily add what is known as the “hidden tax.” This is also known as the “thief in the night” tax, which, on a personal note, is my go-to phrase for this undeclared tax.

The latter seems more appropriate in light of the experience that it leaves a person or household once it is experienced. That is, wages/incomes are received, and then after paying the recurring bills, the individual is left asking, “Where did my money go?”

Welcome to the thievery of the hidden tax, which is more widely known as price inflation.

Under our aforementioned old adage, the central tenet of it is what you make. For most everyday households, this boils down to wage growth rates.

If nominal wages are growing, that is, wages before adjusting for price inflation, it can appear all are getting ahead. Enter the thief in the night tax, and a different story is often displayed.

The nominal wage growth rate is “stolen” via the hidden tax of price inflation.

Inflation-adjusted wages are the only ones that really matter. They assist in providing an answer when contemplating the, “Where did my money go?” question.

Below, let’s take a look for visual perspective.

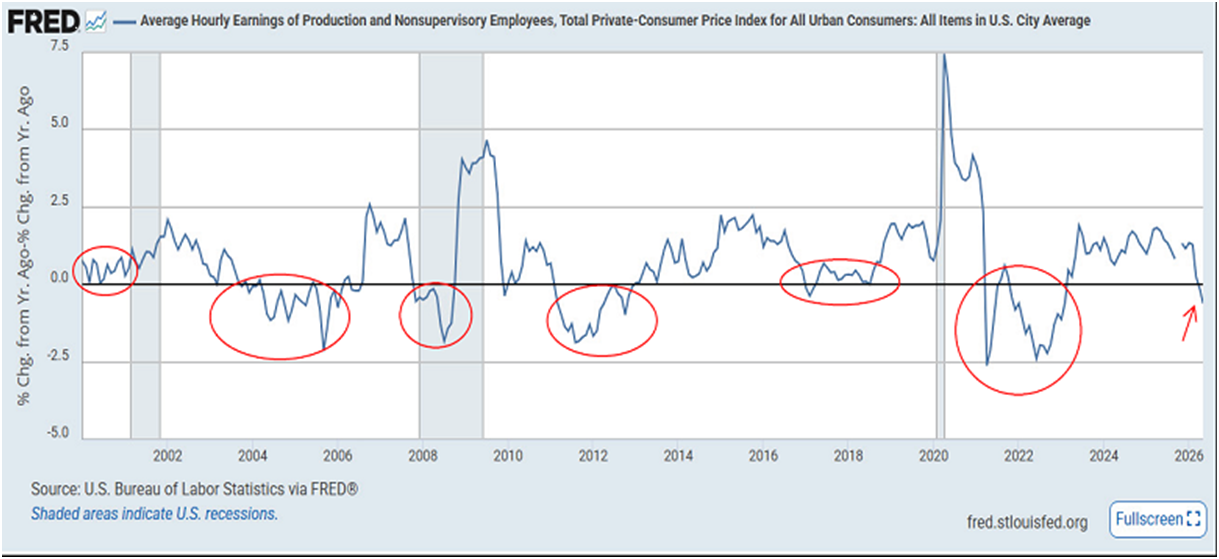

Click for a Larger View: https://fred.stlouisfed.org/graph/?g=1WVtO

Over many editions shared through numerous years we have offered how this 21st century stands out for what shouldn’t be. The above certainly adds to the list.

Note the plethora of red circles.

They are highlighting periods of time within this 21st century whereby wage growth rates, when adjusted for price inflation, were negative, or, in some encircled cases, barely positive.

When looking at them in a cumulative sense, they show up consistently throughout the above timeline.

Unlike headline nominal wage growth, that is, unadjusted wage rates, these adjusted wage growth rates tell a story whereby a tremendous percentage of the working population, at times, has experienced the rate of price inflation exceeding the growth rate of their wages.

They experience how their wages cannot keep up with prices when they go from wage earner to consumer. Over long periods of time, this is not a winning strategy for society at large.

To the far right in our chart above, we placed an arrow denoting that, yet again, we have begun the process of negative wage growth rates.

To the left of our arrow, the large red circle encompasses two years of negative wage growth. After that we saw growth rates went positive in what we could call a mediocre-to-okay level. Positive levels that would not win the day, if you will, especially when negative growth rates were experienced for the prior two years.

Now, to the current day, we are back to negative levels.

If you have a kneejerk reaction that all of this is due to the Iran conflict and will be just fine on the near-term horizon, we offer that price inflation had never been conquered, only tamed, and began its ascent again nearly a year ago.

Along the path of this price inflation era, think 2021 and on, there has always been a reason offered in how the price inflation would be short lived.

Then, when it obviously wasn’t, reasons would surface as to why it had not been short-lived, with a quick follow-on that it would be extinguished soon. Rinse and repeat up to the current day.

There is always a reason, and of course, an underlying narrative to support the reason and how it will be handled soon. The problem? Price inflation continues on.

To be certain, the Iran conflict certainly added to the price inflation storyline, but it is not the only story relative to the re-escalation of price inflation over the near previous year.

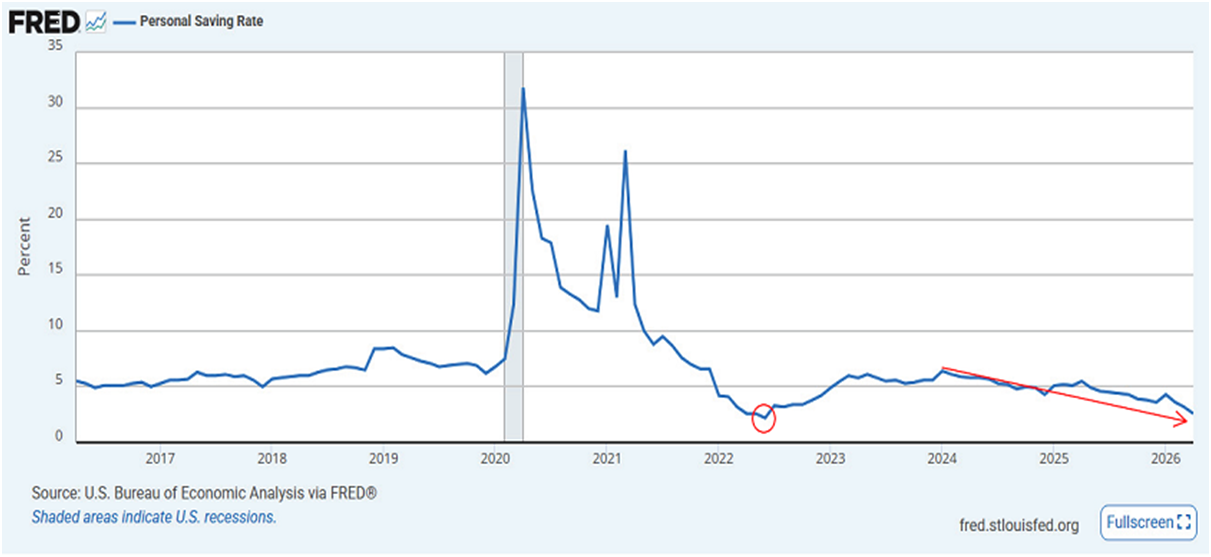

And then there is the savings rate

The logical follow-on of today’s subject is an expected deterioration of the Personal Savings Rate. The proverbial, “rainy day fund.”

Click for a Larger View: https://fred.stlouisfed.org/graph/?g=1WGwG

Above is the Personal Savings Rate depicted over the previous decade. This allows for some broader perspective and yet some recent focus.

Our red arrow highlights the deterioration of the savings rate. We saw a peak level at the beginning of our arrow of 6.4%, which has declined to 2.6% as of the most recent update.

Our current 2.6% level is beginning to rival the ultimate low point of the last ten years, which stood at 2.2% via our small red circle.

While nominal wage growth rates have been consistently positive, the true tell is what wage rates look like when adjusted for price inflation. The adjusted wage growth rates impact many aspects of society and other data points when they go negative, or even marginally positive.

If you want to point to a handful or two of indicators that tell you the real underlying health of the socioeconomic system, adjusted wage growth rates should certainly be included.

Price inflation cannot be tolerated and must be tamed. It has been years now since we have seen the Fed’s 2% target level attained relative to price inflation measures.

While there are many price inflation measures, using the Consumer Price Index (CPI) as one measure, the last time we have seen that post a 2% level or less dates back to the beginning of 2021. That is more than 5 years ago!

Just like now, all along the way, the citizenry was assured that the 2% level would be attained again, often inferring such a level was just around the corner.

We are still searching for that proverbial magic corner. Similarly, now that CPI is registering 4.2% - more than twice the coveted target of 2% - we continue to have narratives offering this is but a blip.

The citizenry, relative to price inflation, needs more than narratives that offer all will be good again – down the timeline. Thus far, in recent years, the various narratives have not panned out to the point of actually ending this price inflation era.

As always, time will tell her story. For now, wage growth is turning negative, again, which, regardless of the reason or narrative, does not work for the everyday household.

I wish you well…

-Ken from Mind Your Stops