More Recession Obsession

June 26, 2025

Throughout past editions we have offered updates of our in-house “recession obsession” issue. As shared previously, recession obsession is easily contracted when deploying capital throughout markets.

Recession itself is not the focal point, but rather, indications of or any sign that recession is coming from just over the economic horizon is the central focus.

Market participants have no interest in waiting around for the economic landscape to be immersed within an economic recess. Said participants are fully focused on anticipation of such an issue, and with this, a redeployment of capital to areas that are treated more favorably once a recession has arrived.

A general description of such areas is that they are defensive in nature. What is not of interest are areas that offer a wealth of risk when recession enters the fray. Risk assets are put aside in favor of defensive areas.

A risk asset is a bit subjective in its labeling. Some areas are marginally at risk, while others get rolled over when recession enters the scene.

If a pullback in economic activity takes hold, revenue and profits can be expected to be negatively impacted for companies at large. Companies deemed to be riskier than others, in good economic times, are at serious risk of significant downside of their bond and stock prices if economic recession appears to be incoming.

Broad Bond Rating Classifications Offer a Scale of Risk

Bond ratings are assigned not based on how they will do if a recession occurs but rather on how they are rated on a risk spectrum as the economy is performing. Said differently, bond ratings are offered in the moment, if you will, not as a prediction of how risky they are if a recession arrives.

With this, we can offer the higher-risk bond categories as good canaries to aid in assessing collective participants concerns and expectations of a near-term recession.

Like the historical use of canaries in coal mines, if the canary begins to labor in its breathing to a point of falling over, rest assured, the air quality is diminishing rapidly. Similarly, participants pricing behaviors within higher-risk bond categories act as one of many economic canaries.

What adds credibility to the higher-risk bond canaries is the fact that they are traded in the smartest market. The bond market is often viewed as the smartest market, generally speaking.

Bond participants, by the nature of their underlying trading vehicles, are forced to be deeply focused on many areas of the socioeconomic landscape. When they show concerns, you should take note regardless of whether other markets seemingly do not register said concerns.

Conversely, when other markets show concern but the bond market seems not to care much, you should also take note. Other markets, think the stock market as an example, get top billing in reporting, and with this is often viewed as the most important market in terms of its messaging. Bond market messaging is our first go-to.

Junk Bonds

Our recession obsession has us continually dialed into anything that will aid in offering incoming recession is increasing in probability.

We could trot out a number of observation points to share here from within the bond market, but to keep it customarily succinct, we share the High-Yield bond segment. This segment is also known in slang as “junk bonds.”

They retain the labeling of junk because their ratings offer a high risk of default, and through this, for our purposes within this edition, a canary of expected economic conditions in light of their sensitivity to the overall health of the economy. Through this, their messaging via pricing behavior can simply offer recession concerns are increasing or decreasing.

Importantly, this says nothing about the quality of the economic structure. For example, and this is important, if you knee-jerk a mental thought that offers something like, “Yes, the economy is holding up, but all this debt supporting it has us heading toward ultimate doom.”

This segment of the bond market (our canary known as junk bonds) doesn’t care about the structure per se. They care about getting paid. This may sound harsh, but it is the reality.

(Inherent to this is part of the beauty of watching this segment as an economic prognostication tool. That is, this “tool” is direct in its messaging. Health of the longer-term U.S. fiscal structure is more the Treasury bond market’s concern than it is this segment’s concern. That is a different topic that we have shared in past editions and will continue to address in future editions. But for this edition, with this question in mind – think, our recession obsession – the bottom line is the focal point: recession or no recession in the near term?)

Junk-rated bonds pay a higher interest rate in light of their higher risk of default.

With this said, participants are willing to hold and acquire more if they feel the economic backdrop is healthy enough to keep them from rolling over via a recession. The higher default risk is their concern, in that the higher interest rate is their attraction. They want to make sure they will get paid the higher rates they are seeking.

An inbound recession places default risk at a very high level for these risky offerings, which would offer a double negative to participants. That is, loss of principal and interest payments.

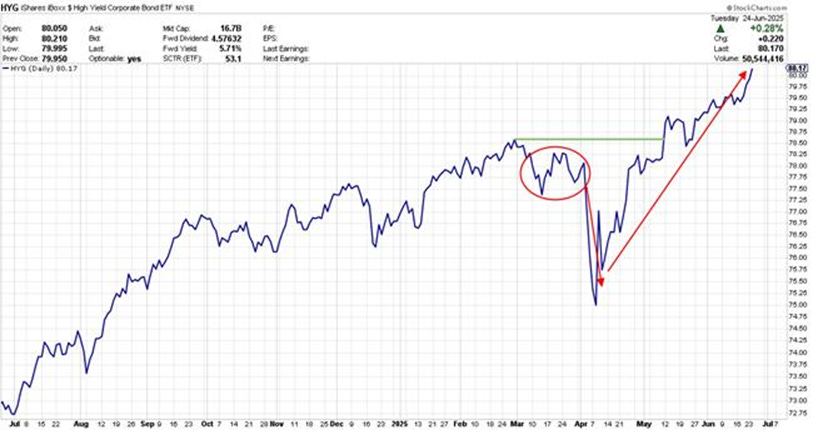

Click For Larger View: https://schrts.co/DdhgYSFw

Above is a one-year chart of a high-yield corporate bond vehicle on a price basis.

We have placed a few lines within the chart to point to messaging since our last sharing of this back in late winter.

Our green horizontal line denotes the high price mark dating back to late winter. Our red circle, just below it, highlights pricing behavior in the month of March. We highlight this in particular, again viewing this through the lens of an incoming recession watch, because we were very focused on this bond market behavior back then.

While the stock market was taking on notable downside while seemingly anyone with a microphone was offering, “Recession is coming!” due to tariff policies, we could not help but notice the relative lack of concern in this high-risk corporate bond market segment.

The above pricing behavior, interestingly, was corroborated by triple C’s behavior – an even riskier segment of the corporate bond market. These areas were not offering recession. Their relative outperformance was notable.

Our red down arrow in the first week of April noted their chiming in with increased recession concerns. This while other markets were putting on massive downside with extreme volatility. Again, the relative outperformance of these high-risk corporate bonds kept our attention.

Far more notable is their behavior since the first week of April. Per our red up arrow, this high-risk junk bond space catapulted off its lows and has not looked back. Note how it rapidly trended back up to its previous high point (green horizontal line) and continued on from there.

In the far right we see this space has continued to put on a series of higher highs – THE definition of a solid uptrend.

To the point of our recession obsession: In totality of the above pricing behavior, most notably the uptrend behavior since early April, offers there is no concern from these participants of near-term recession.

Bidding up this space to continual higher highs is not the behavior collective junk bond participants display if they expect economic issues near-term. This is corroborated within other higher-risk areas of the corporate bond market as well. We will continue to watch and share accordingly.

Fourth of July Talk Already?

As we look at the calendar, along with our typical publishing schedule, we see next week offers little room for an edition. Next Friday is the Fourth, while Thursday markets close early, representing the early shutdown by society at large of the midsummer break that coincides with the Fourth of July. We wish you some enjoyable downtime. See you the following week of this midsummer holiday!

I wish you well….

-Ken from Mind Your Stops