Let's Call it a Six-Month Checkup

June 4, 2025

Back in the summer of 2023 we decided to finally open up the topic of a major historical shift in the bond market. The shift was a change in a long-standing trend, i.e., a megatrend, as we referenced it.

Bond market participants dramatically changed, on a trend basis, what interest rate they need as fair compensation to hold the well-known benchmark 10-year Treasury note.

We say benchmark because it is used as a benchmark interest rate and can play a role in setting other interest rates within the financial system. Offered simply and succinctly, the 10-year yield and its trend are a big deal that should always be noted.

By the time we opened up this topic, back in 2023, it had already been a year in the making. We ourselves thought some time should pass to help ensure this wasn’t some sort of a knee-jerk response that turned out to be an aberration of the long-standing megatrend.

Along the timeline, we have intermittently checked in on this developing storyline by sharing it within editions. It has been nearly six months since we last shared an edition on this market topic, so we thought it timely to check in again.

Megatrend Shifts Are Difficult Psychological Adjustments

Shifts in megatrends are difficult to psychologically grasp in light of their established long duration, as said duration has them entrenched as part of the fabric of the socioeconomic landscape. Also, in light of their length in time, they also become multi-generational, which further entrenches them within the societal backdrop.

They become so entrenched the masses rarely, if ever, even question that it could be any other way – it is all we know – how could it change?

This is particularly true for the relative youth of the multi-generational makeup because it is literally all they have ever known. To suggest to them it could be different, vastly different, seems laughable, if not outrageous.

Importantly, throughout history, all trends change, even the megatrends.

The Bond Market Continues to Offer this Megatrend Is Over

Bond market participants adjust yields (think interest rate) for notes and bonds by bidding prices higher or lower. If bond market participants believe X bonds should be offering a higher interest rate, said bonds will be bid down in price within the bond marketplace.

As bonds move lower in price, their yield (interest rate) moves upward. For whatever reasons, usually many reasons, bond market participants feel the bonds in question need to pay a higher rate to offer fair compensation relative to the risk a participant takes on to hold them.

Keeping this very simple, this is no different than if you as an individual agreed to loan money to X person or entity. Assessing the general risks of the loan is how you would determine what level of interest rate you would need to receive to compensate you for the risk of loaning out your money and holding their note/bond in your possession.

Taking this just one step further, to offer an experiential understanding here, if you then offered this bond for sale to X person or entity (think, you just took it to a “marketplace”), they would do an updated assessment of risks, and upon doing so, offer you a lower amount than the face value of the bond.

With their lower offer, they are determining risks have increased and they need to receive a higher yield (interest rate), so by offering you a lower amount than face value, the stated interest rate to be paid, as listed on the bond agreement, will yield a higher rate to the new owner in light of them having paid less than the face value of the bond.

This is how market participants “change the interest rate,” if you will, of an already issued bond. By bidding the price lower, the bond’s contractual stated interest rate yields a higher rate to the new owner.

Click For Larger View: https://schrts.co/gNJcHRFA

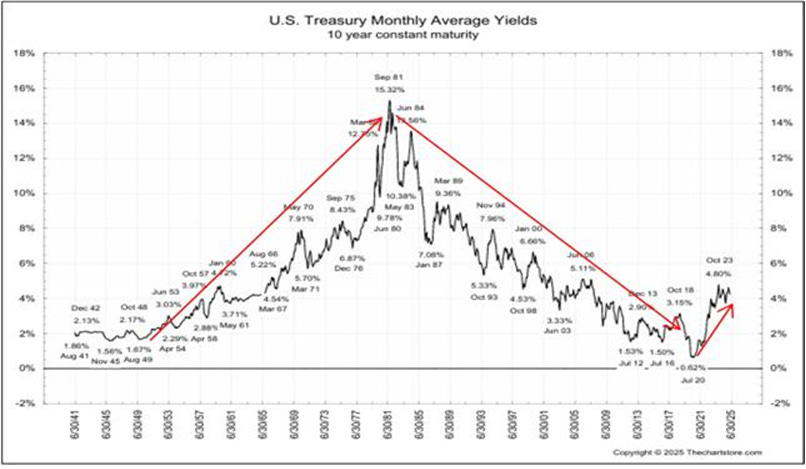

Above is a nearly 50-year chart to fully depict the megatrend for 10-year Treasury notes that had been in place since 1982. Per our well-established red downtrend line, we can see interest rates continued to trend lower and lower over time.

Importantly, like all trends, the above trend consistently offered an ebb and flow whereby rates would move lower, then would offer a trend attempt upward, only to be turned back with an even lower interest rate prevailing. Over decades, this megatrend stayed in place as ever lower rates unfolded.

Looking to the far right portion of the chart, we see this all began to change in 2021 with a violent upturn.

The above multi-decade trend behavior changed notably. Bond market participants were pushing prices consistently lower as they were requiring higher yields to compensate for X risks of holding these notes.

Then, as we crossed into early 2022, participants did what they were not able to do since 1982; they took out the downtrend line as they pushed interest rates easily up through said line.

From 2021 on through 2022, note the overall powerful change in behavior. Interestingly, this is often how true trend changes occur. That is, powerfully in their newfound direction.

Interestingly, a powerful shift in the opposite direction further adds to a general belief that what is unfolding is a short-term, knee-jerk-type reaction to X scenario.

Relative to megatrends ending, this is especially true because, as shared earlier, it just doesn’t seem possible that said trend can be over.

Shared to the point, bond market participants are offering the multi-decade downtrend in interest rates is over.

This does not mean interest rates will never move lower, but rather a series of ever lower rates is what has ended, per their trend messaging. With this, a series of ever higher interest rates, over time, (i.e. a new megatrend), is shaping up to be in place.

We continue to share this storyline, on occasion, in light of its ongoing behavior, which is pointing toward a new megatrend that has indeed begun, circa late 2021.

The Mid-1940s

Back in the mid-1940s, a new interest rate megatrend had begun whereby interest rates found a way to move higher as the years ahead turned into decades. As shared earlier, within trends, to include megatrends, there always exists an ebb and flow of the trend.

In the case of the mid-1940s launch point of higher interest rates, there were times along the path where interest rates turned notably lower, which at the time could have easily been construed as the end of the higher interest rate trend.

Through the process, the megatrend line itself was never broken (offering the trend remained intact), with interest rates ultimately finding a way to move to an even higher level.

As offered, all megatrends find their end point, which, in the case of the 40-year trend of higher rates dating back to the 1940s, witnessed its end circa 1982.

Once we entered 1982, few could comprehend that interest rates had begun a new multi-decade process of finding a way to move ever lower. This seemed an outlandish suggestion by anyone offering such a view.

All society had known for decades was a process where interest rates found a way to move higher. Evidence presenting itself that said interest rates were going to change direction, not only on a trend path but also on a multi-decade timeline, surely was met with ridicule.

Above is a nearly 90-year chart of the ten year Treasury note on an interest rate (yield) basis.

Focusing on our left upward red arrow, we see what this interest rate had done, on a trend basis, dating back to the mid-1940s. Note the ebb and flow, which is to say, rates moved higher, then moved lower, and then higher again. Through the process, rates trended higher as rates moved upward to higher high points.

This underlines our earlier point that offering a new megatrend has already begun does not mean we will never see interest rates move lower. What it offers is the trend of ever lower rates - yes, that 40-year megatrend, has concluded.

I wish you well…

-Ken from Mind Your Stops