Checking in on Price Inflation

July 16, 2025

It has been a while since we offered an edition on price inflation, so we thought it timely, given the Consumer Price Index (CPI), along with its universe of subcomponents was updated yesterday.

A few months ago, we posted an edition on this topic in the midst of raging tariff narratives that offered a certain outcome of spiking price inflation. At that time, we offered that it was far too simplistic of a conclusion relative to the complex topic.

It suggested, drilled down to simplicity, that end consumers would offer zero pushback relative to any increase in prices. Our larger view was that corporate profit margins were more at risk of a reduction compared to the narrative certainty that systemic price inflation would be spiking.

The profit margin reduction view arises through the lens of companies at large having to eat X percentage of any tariff increases in light of their inability to pass through said costs to consumers. This, in light of their desire to maintain market share and their unwillingness to risk general demand reduction via consumer pushback of tariff-induced higher prices.

The spiking price inflation narrative essentially offered any company, regardless of its industry, would be able to simply tack on an X percentage tariff increase onto their existing price, and in so doing, they would easily maintain their profit margins, along with their market share, without missing a beat.

What was missed in the narrative builds were consumer behavior considerations. What was also missed, drilling down a bit, were demand characteristics relative to X company and the industry they operate within.

To treat all companies across all industries as exactly the same, relative to how their end consumers view them, leans into comedy.

The applicable econ lingo is the elasticity and inelasticity of demand. Both demand descriptions are easily recognized by all of us consumers.

Fret not, this is as techie as we will get on the econ lingo front.

Simply, elastic demand offers price leads to a change in demand.

Companies at large deeply understand this and are aware of their business risk relative to pricing. Young kids also understand this when they price their lemonade at their street-level lemonade stand. Increase that price too much, and sales volumes fall accordingly.

Elastic demand informs us that we consumers are sensitive to price. If prices increase when our demand is elastic, then our demand for goods and services wanes in light of the higher prices.

To offer or imply via X narrative build that X tariff increase will equate to an automatic certainty of X systemic price inflation increase suggests we consumers have no elasticity in our demand of goods and services. Said differently, and in keeping with our econ lingo today, this would mean all demand is inelastic. That is nonsensical.

If this were even remotely true, this would offer a frivolous discretionary consumer item (an elastic demand item, if you will) is as important to us as, say, heating oil is in the middle of a polar vortex episode in the middle of winter. One plays a vital role in keeping us alive, while the other is a general trinket, or thereabouts.

Essentially, companies have to assess how elastic or inelastic the demand for their goods and services is and then figure out how much, or how little, profit margin impact they are willing to incur. Of course, there is always competition to consider in this assessment as well.

It does not boil down to such an easy narrative that X input cost increase equals a guaranteed X increase in the end price of goods and services, and hence, systemic price inflation.

The Updated Data

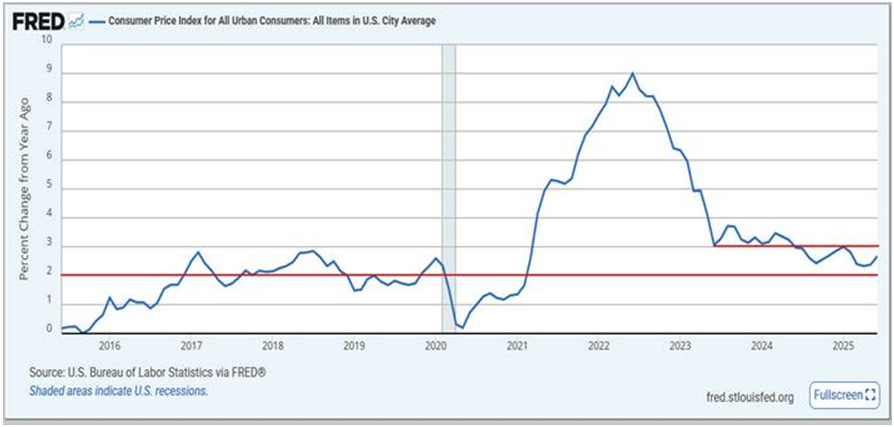

Click For Larger View: https://fred.stlouisfed.org/graph/?g=1KCfq

Above is a decade view of the CPI expressed as a percentage change from one year ago. We have inserted two red horizontal lines to denote important markers.

First, our lower-level red line encompasses the entirety of the chart and is meant to act as a visual for the well-recognized Federal Reserve’s 2% inflation target. Prior to the price inflation era we have been living in over recent years, we can see that when CPI went north of 2%, it would generally drift back down to the 2% level and below.

To the far right of the above chart, we can see our current results continue to remain stubbornly above the 2% level.

Importantly, focusing on our second (shorter) red line, CPI was refusing to penetrate through the 3% level, which was acting as a floor, but over the previous twelve months, the 3% level has continued to act as a ceiling.

The bottom line of the above results is that we continue to experience a range for CPI. That is, we remain north of 2% and yet south of 3%, i.e., a range. Clearly, and importantly, this range offers no spike in price inflation to date.

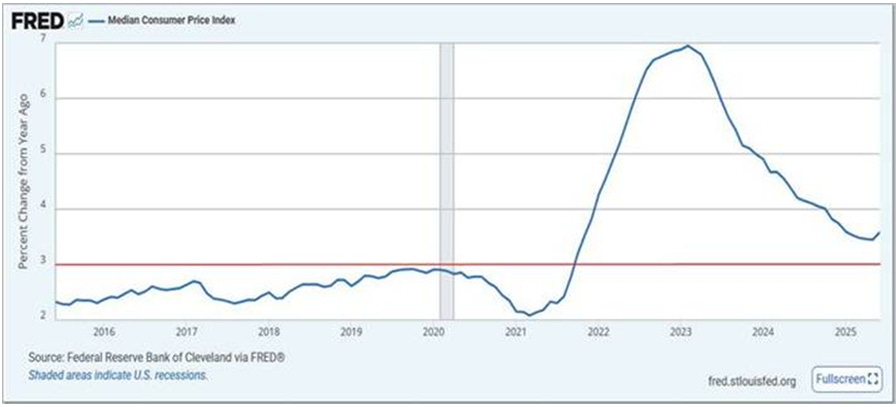

Click For Larger View: https://fred.stlouisfed.org/graph/?g=1KCj2

Above is another look at price inflation via the Median CPI calculation from the Cleveland branch of the Federal Reserve system. This is one of our favorite measures for price inflation generally because it digs into the depths of the systemic pricing landscape within the U.S. economy.

The above is also a decade view in order to offer some recent historical perspective.

Our inserted red line denotes the 3% level, as that level has been a line in the sand prior to the 2021 price inflation breakout.

Note how we remain well north of the 3% red line with little attempt, at this stage, to touch its level, let alone penetrate through it and hold, as in prior years. Our current reading comes in at 3.6% - well north of 3%.

The bottom line of all of the above is we are not experiencing the well-advertised expected spike in price inflation to date. In addition, the price inflation storyline continues to show itself, albeit at a lower level than in recent years.

Deeper within the pricing landscape, as depicted with the Median CPI (second chart), we can see price inflation, systemically, remains a challenge.

A wealth of progress has certainly been made, in particular over the previous year-plus, but to say this price inflation era has come to a close is certainly premature. More progress is needed.

I wish you well….

-Ken from Mind Your Stops