An Employment Market Observation via Stock Market Participants

February 26, 2026

Within a late summer edition of 2025 followed by an edition in the fall of 2025, we shared how collective stock market participants were displaying concerns for the employment market via the payroll processors.

The payroll processors are quite sensitive to the health of the general employment market in light of their core business function being at the epicenter of servicing employed personnel.

In light of market participants’ obsession with pricing markets today, in light of what they see downstream on the economic timeline, we found the behavior of the processors’ stock prices worth noting at those times.

In the front part of 2025, two long-standing payroll processors were clear stock market leaders.

Underlining their market-leading resilience, when the stock market went hard south in March and part of April, these processors stood out in that they barely went negative on their year-to-date performance at that time.

It was interesting to observe their resiliency in that collective market participants were clearly not concerned about the prospects for the downstream employment market, as they were extremely reluctant to trade their share prices lower. This, while large swaths of the stock market fell with ease.

Tariff implementations back then had collective participants concerned for general share prices, but not for the payroll processors.

It was as though they were signaling that the reindustrialization attempt with tariff implementations, or the onshoring attempt, as it is also referenced, would be a net positive for the general employment landscape, given time.

We have continued to observe how market participants are trading these two well-established payroll processors’ shares and continue to be amazed at the tremendous turn in the pricing of their shares over the previous nine months.

To go from tremendous resiliency in the face of notable downside stock market pricing to then being tremendous underperformers within a few months, all while the general stock market landscape improved notably, is a rapid change in tone in how their shares are being priced by market participants.

This is a multi-decade change in behavior

Over recent decades the payroll processors have lined up quite well with the general trends of the stock market. As the stock market would ebb and flow, the processors would trade accordingly.

This relationship was never lined up perfectly, but that is to be expected. It is the general trend of them that has stood out through recent decades. With this long-standing trading relationship solidified for such a long period of time, their divergence stands out notably.

Below we look at two charts that underline this divergence.

Click For Larger View: https://schrts.co/daAnceaG

Click For Larger View: https://schrts.co/PebwSsQY

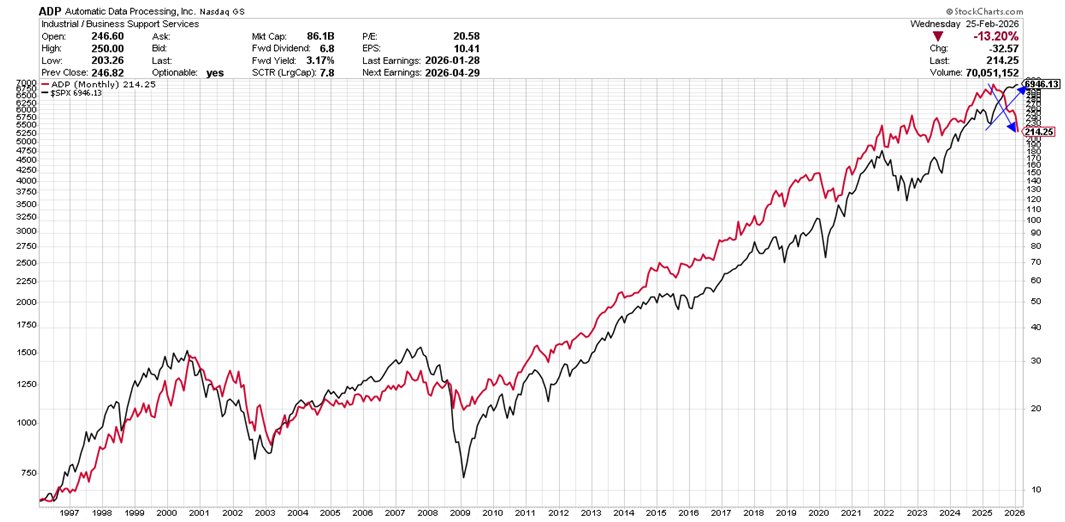

Both of the above are monthly charts that date back 30 years to 1996. In both charts the black line represents the S&P 500, while the red line represents each payroll processor.

In the first chart, the red line is Automatic Data Processing. In the second chart the red line is Paychex. As a side note, we are using both as tools for this edition. We are not advising a buy or a sell on either of these companies.

Note the general trending correlation of both over the decades to that of the S&P 500. At times there is notable outperformance by the payroll processors, be it to the upside or the downside in that they would not go down as much as the S&P 500.

Our focal point for this edition is the far upper right of each chart.

We have noted the tremendous divergence in pricing behavior of these two long-standing payroll processors to that of the S&P 500 via our blue trend arrows.

The divergence has been stark in contrast as the S&P 500 has trended upwards while the processors have trended down since the summer of 2025. This continues in the current day.

Below, let’s take a look at this divergence in closer detail.

Click For Larger View: https://schrts.co/PnYPFZMD

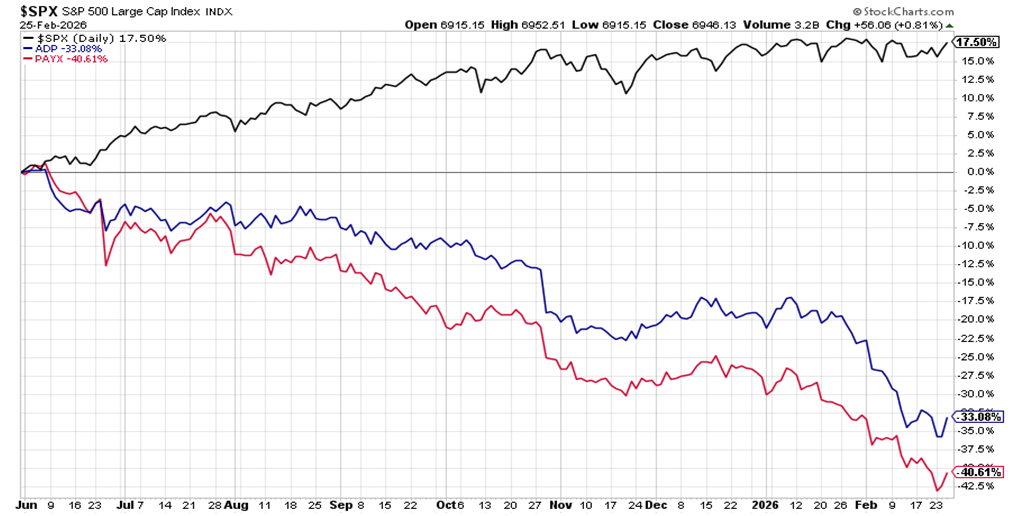

The above is a returns chart that dates back to June of 2025 for the two payroll processors. The blue and red lines are the processors, while the black line represents the S&P 500.

The trading relationship of the processors to that of the stock market for the past 30 years gives the chart above its “wow” moment, if you will. To see this level of negative divergence is eye-opening.

Since June of 2025, think nine months, while the S&P 500 went on to solid double-digit growth, the processors are down 33% and 40% each.

Per the 30 years of trading history, we have not seen collective market participants display such a concern for the payroll processors (relative to that of the broad stock market), and, through them, a concern for the prospects of the employment market such as we are seeing in recent time.

Market participants are displaying a consistent disinterest in these companies while simultaneously choosing not to display a general concern for the stock market at large.

This is interesting in that if said participants had a notable concern for overall economic activity, the stock market at large would at least show some deterioration.

Does AI need payroll processing?

Most are well aware of the growing realization that Artificial Intelligence (AI) is here and that this technology, like most technological progress, will be disruptive. In this case the disruption can be, and seemingly is expected to be, very disruptive to a vast array of areas within the broad employment landscape.

By most accounts, this technology will be impacting nearly every job classification, given time. How much time? That is unanswerable with any degree of certainty.

AI represents an unknown and yet seemingly vast labor pool ready to compete for employment opportunities. Companies at large are certainly incentivized to employ AI, realizing that payrolls are a significant line item within their profit & loss accounting statements.

In a Financial Times interview recently, speaking to our “how much time” question above, Microsoft’s AI CEO said most white-collar jobs can be fully automated within the next year or two.

Time will tell her story on this, but for now the above divergence displayed by market participants toward payroll processors, relative to the behavior of the broader stock market, is offering their caution toward the employment landscape. The AI question is certainly playing a role in participants’ reluctance to bid these companies higher.

The obvious feedback loop question is, if the employment market turns upside-down whereby employment growth (for humans) is marginal, how does the economy hold up?

Through this question we cannot help but wonder if the payroll processor pricing behaviors (displayed above) are a very early sign of things to come for the stock market at large.

This is not a downstream expectation as much as it is a curious contemplation when thinking of the potential ability of AI technology to massively disrupt the employment landscape.

If this unfolds into decimating large swaths of employment opportunities, that level of disruption will show up in the broader stock market.

As the old adage goes, may you live in interesting times. We all are certainly living in interesting times eh.

I wish you well…

-Ken from Mind Your Stops