A Recession Watch through the Lens of the Bond Market

July 1, 2026

It has been awhile since we offered an edition relative to any type of recession watch.

There are numerous angles that can be taken when discussing the potential for an incoming recession. One of our favorites is to study the bond market to see what collective participants are offering via their pricing and trading of various bond categories.

This approach itself invites a plethora of angles in light of the various bond categories. This, along with the use of relative strength charts within the space, adds additional layers for perspective.

It is important to keep in mind that market participant messaging offers insight into what may be coming down the pike, not what X data point(s) are offering in the now.

Market participants have no interest in waiting around for the economic landscape to be immersed in data that is pointing to an imminent recession. Said participants are fully focused on anticipation of such an issue, and, with this, a redeployment of capital to areas that are treated more favorably once a recession has arrived.

A general description of such areas is that they are defensive in nature. What is not of interest to said participants are areas that offer a wealth of risk when recession appears to be on the horizon. Risk assets are put aside in favor of defensive areas.

A risk asset is a bit subjective in its labeling. Some areas are marginally at risk, while others get rolled over when recession enters the scene.

Cutting to the chase of our observation for this edition, let’s take a look at a couple of areas within the bond market that historically get rolled over when recession enters. In other words, these are not marginally at risk but rather are lathered up in risk, in particular when recession concerns arise.

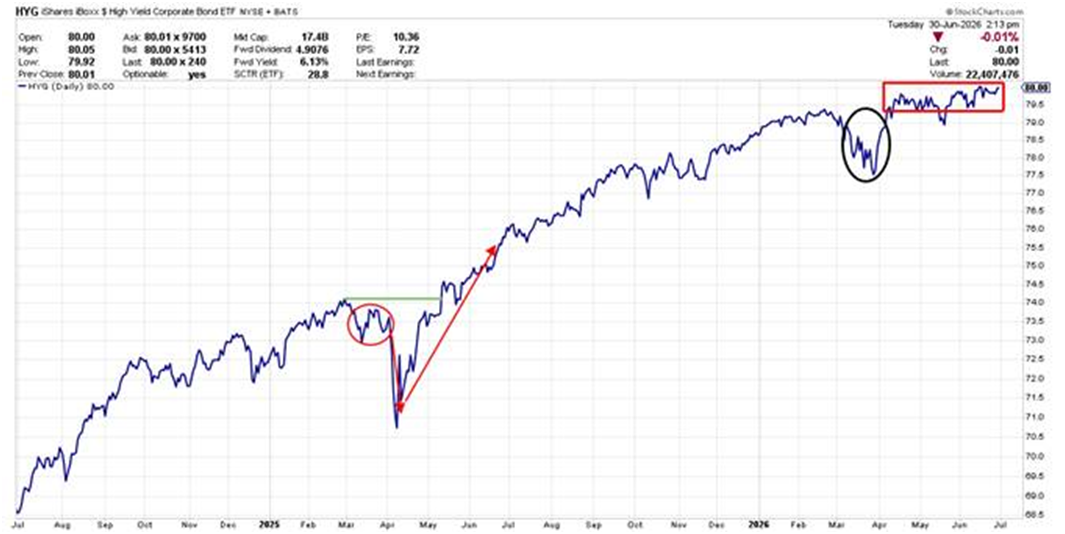

Click For a Larger View: https://schrts.co/QZFYgeGr

Above is a two-year chart of a high-yield corporate bond vehicle on a price basis. We have added a few annotations to draw attention to how skittish bond market participants can be with this higher-risk category when concerns of recession increase.

We begin with our first red circle and follow-on uptrend arrow approximately mid-chart.

This was in the spring of 2025. Recall how at that time the tariff debate was all the rage. With that debate came increasing concerns that recession would result.

The stock market, as a risk asset category, began to fall earlier and harder than the above high-yield corporate bonds did in the early weeks of that process.

For their part, bond market participants were not as sure that recession would be an end result. Ultimately, the above high-risk bond category chimed in with downside pricing but to a lesser extent than the stock market.

To the far right we have placed a black circle on some more recent downside with this bond category. This is the initial period of time when the Iran conflict began, which raised downstream economic concerns.

In follow-on weeks these bonds were bid upward again, offering little concern of economic issues via bond participant pricing of this high-risk category.

To the current day, we have placed a red rectangle to highlight the pricing behavior of this category in recent months. Note how stable the pricing behavior is in this time period.

Participants within this high-risk bond category are showing little concern of recession issues entering the near-term fray.

Below, let’s take a look at an even higher-risk bond market category to gain additional recession perspective from bond market participants.

Click For a Larger View: https://schrts.co/dKkYFBPj

The above is also a two-year chart with similar annotations included as in our first chart.

This category of high-risk corporate bonds is known as the “Triple Cs.”

We often say that the issuers of triple-C-rated debt are one mistake away from needing life support. We offer this to underline their risk status.

Adding broad economic recession to the business landscape places these bonds at significant additional risk. Hence, participants have no appetite for this bond category if they suspect economic issues are on the horizon.

Just as in our first chart we have annotated how these bonds react if economic concerns of any type enter the scene.

The above category responded to both the tariff debate of early 2025 and then the upstart of the Iran conflict in early 2026 by dropping in price significantly and quickly.

To the current day, just as in our first chart, note our red rectangle which depicts the stable pricing of this bond category by participants in recent months.

For this highest of risk bond categories to display such pricing stability of late, it offers collective bond market participants are showing little concern of a near-term recession.

Importantly, as depicted in both of the above charts, increased concerns of an incoming recession by participants do not assure a recession as a certainty. There are additional tools to help forecast the odds of recession certainty.

A starting point of doing a recession watch through the lens of the bond market is to observe the pricing behavior of the higher-risk bond categories, such as we have above.

The message to this point in time, via pricing from participants, is that economic recession is viewed as a low probability in the near term.

Fourth of July Already?

It is hard to believe the 4th is essentially upon us. We wish you some enjoyable downtime with the midsummer break this national holiday brings with it. We will share another edition as early July unfolds.

I wish you well….

-Ken from Mind Your Stops